Governing blockchain treasuries

Using new comparative economics to understand the governance of collective treasuries

Governing collectively-owned blockchain treasuries must trade-off the threat of expropriation from dictatorship (e.g. founders, foundation members) and disorder (e.g. hacks, colluding token holders).

Public goods are typically understood to be funded and provided by governments (who tax and spend to provide theoretically under-provided goods). The long-term sustainability of blockchain ecosystems requires funding of ‘local public goods’ such as research (e.g. on protocol security), innovative projects (e.g. bridges and wallets) and marketing (e.g. education for new users).

Blockchains need public goods but they don’t have governments. And so blockchain communities often create a treasury: a pool of collectively-owned cryptocurrency for the purposes of funding public goods.

Today’s blockchain treasuries are large, loosely-defined and often scantly spent. This is an institutional design problem. What is the optimum size of a treasury? How should it be funded (e.g. a pre-mine of tokens or from on-going fees)? Should the treasury remain wildly native-token undiversified, or should we diversify into other assets? What assets, and how?

These questions all tightly relate to the problem of treasury governance. Today the blockchain treasury ecosystem has evolved an ad hoc assortment of funding mechanisms and governance structures. Those governance mechanisms include founders’ multi-sigs, non-profit foundations, grants programs and proposal processes, angry discussion forums, and of course the inevitable attempts to create treasury DAOs.

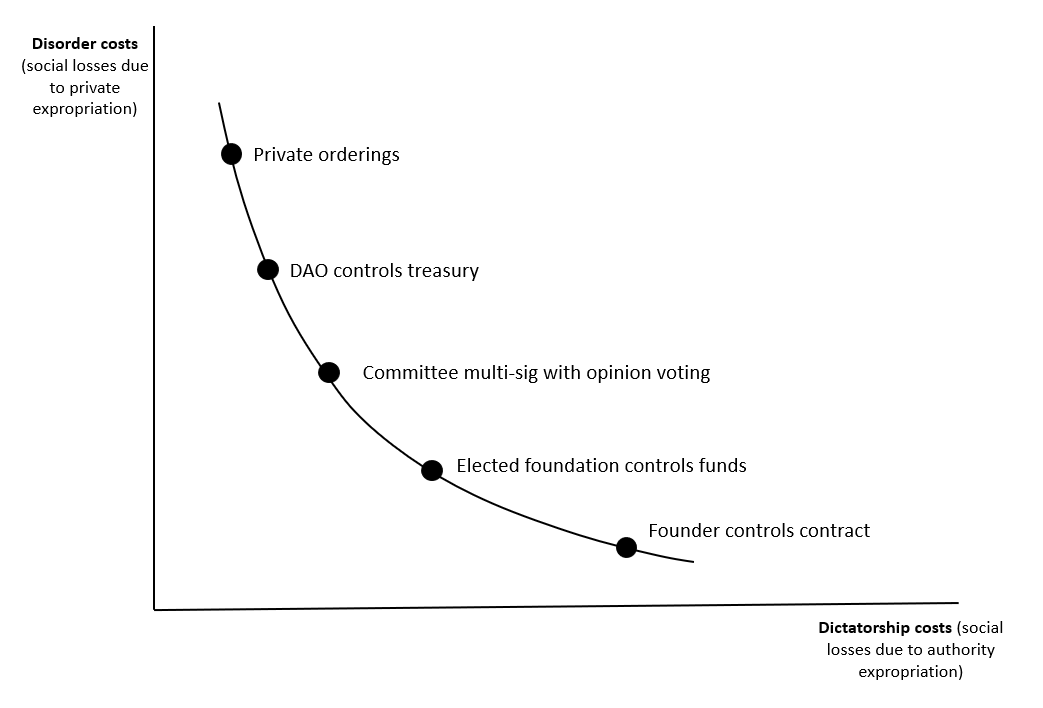

The fundamental problem underpinning collective treasuries can be understood through the lens of new comparative economics and the institutional possibility frontier (IPF). The IPF was designed to understand institutional design for the social control of business (e.g. state ownership versus regulation versus self-governance). This framework enables us to conceptually compare different institutional possibilities in how their ameliorate two social costs: the costs of dictatorship that arise from state expropriation of property (e.g. excessive taxation or force), and the costs of disorder that arise from private expropriation of property (e.g. theft, violation of contracts).

The IPF is a (convex) curve of institutional possibilities representing different combinations of dictatorship and disorder costs. Implementing institutions to control the costs of disorder increases the costs of dictatorship, and vice versa. Different societies have different institutional possibilities owing to their underlying norms, culture and civic capital, thereby giving different IPF curve shapes and dynamics.

While blockchains don’t have governments, we can use new comparative economics to inform blockchain treasury design.

Dictatorship costs in the governance of blockchain treasuries typically arise from those in positions of authority expropriating their funds for their own purposes. Blockchains are not born decentralized, and their treasuries don’t tend to be either. The most obvious dictatorship cost is that of a founder controlling a pre-mine of a treasury and stealing the funds. More broadly, individuals in positions of authority (e.g. foundation members) impose the threat of dictatorship costs (e.g. misuse of treasury funds). Nevertheless, these positions of authority do reduce the costs of disorder.

Disorder costs in the governance of blockchain treasuries arise from the open nature of these ecosystems. The most obvious disorder cost is that of an individual discovering a bug in an on-chain treasury contract and syphoning off funds. More broadly, many blockchain treasuries enable public proposal processes and voting mechanisms on how to spend treasury funds. Those processes—particularly with low participation rates and sometimes automatic execution of vote outcomes—open up disorder cost attack vectors. They do, however, reduce the costs of dictatorship.

Different treasury governance mechanisms map to different points within the IPF space (see below). A founder-controlled treasury, for instance, has theoretically higher dictatorship costs (and low disorder costs). A multisig contract together with non-binding stakeholder voting has theoretically lower dictatorship costs (and higher disorder costs). A fully DAO controlled treasury, with automatic dispersing of funds through on-chain voting, lowers the cost of dictatorship (but increases the costs of disorder).

Two points are worth nothing about the framework. First, the IPF space is open to institutional innovation. We are currently seeing a new and diverse range of treasury governance structures being developed that deal with disorder and dictatorship costs in new ways. Some interesting (existing and planned) mechanisms include budget periods with built-in incentives to spend the funds during those periods (e.g. see Polkadot), automatic execution of funding through a DAO and on-chain voting (e.g. see Dash), and unique voting rights such as liquid democracy and delegation of voting rights (e.g. see Cardano). Each of these mechanisms—as well as others such as vesting periods, proposal fees, quadratic voting, foundations and so on—are attempts to control the dual threats of dictatorship and disorder in a blockchain treasury.

Second, the treasury governance problem changes over time as the blockchain ecosystem develops. Early in the development of a protocol, a low-value treasury and a close trusted network of team members the ‘efficient’ governance of a treasury may well be through a tightly-held multisig. As a protocol develops, a high-value treasury and an increasing number of external stakeholders may mean the ‘efficient’ governance of a treasury is through a DAO or a more formally elected non-profit foundation. Indeed, we can begin to analyse how the IPF shifts and empirically compare different ecosystems (such as the rough representation below).

The frontiers of collective treasury governance are not well understood. Not only are many of these treasuries terrifyingly large (multi-billions of dollars), the trade-offs about how to govern them are not well understood. New comparative economics and the IPF provide us a framework to understand and compare the trade-offs in these design choices. That understanding is underpinned by theoretical development together with close empirical observation of the build-out of blockchain treasuries (and controversies).

This post comes from joint research with colleagues at the RMIT Blockchain Innovation Hub on related treasury governance topics including Chris Berg, Sinclair Davidson, Aaron Lane, Trent MacDonald and Jason Potts. See our recent working paper on SSRN, ‘An Economic Theory of Blockchain Foundations’